Outsized Gains Are Commonly Seen at the End of a Market Bubble

Chief Investment Officer Eric Peters worries that the stock market has gotten ahead of itself. He stops short of calling it a market bubble, but he warns that accelerated gains could have dire effects on portfolios everywhere.

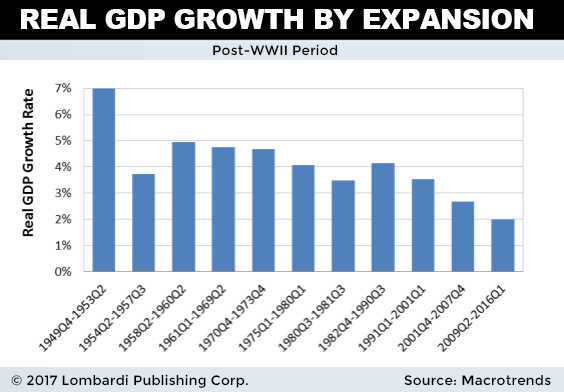

Peters notes that while “nerds,” on average, forecast a three-percent annual gain on the S&P 500, it has increased 10% in the first half of 2017 alone. Unlike previous times when the market had room to run, this isn’t the case this time. “Today the trailing P/E is roughly 26, with overnight rates 19% below the 1982 levels, and 4.5% below the 2000 levels… so we’re obviously not at a similar point to 1982,” said Peters. (Source: “Hedge Fund CIO: “We’ve Realized Roughly 3 Years Of Gains In The First 6 Months Of 2017”,” Zero Hedge, July 16, 2017.)

Advertisement

Also Read:

Hedge Fund Manager Eric Peters Predicts Stock Market Crash in 2018

Of course, Peters is right. Unlike those times when the market ran, valuations were much less sanguine. Even more importantly, there was tremendous latent economic growth potential once interest rates were reduced. There’s no such potential today. Eight years of rock-bottom rates have unlocked all the consumer and commercial investment demand it could, and there’s little possibility of stimulating demand further. Not just present demand either. Ultra-low rates have pulled a tremendous amount of future demand forward.

But in his view, the real risk to investors doesn’t necessarily involve a market crash. Rather, the more likely risk is low 10-year returns. “You rally so much that your 10yr return forecast turns flat. At which point you could go sideways for a decade,” said Peters. (Source: Ibid.)

A scenario with zero percent returns every year would give most investors nightmares. But that’s not how the stock market works. The market doesn’t just stay flat over an extended period of time. It fluctuates and oscillates from one extreme to the other. If Peters thinks 10-year returns could equal zero percent, he’s effectively calling for a stock market crash. Peters is inferring the likelihood that one or more of those years will return deeply negative double-digit returns.

It’s anyone’s guess whether two years yielding -17% and -12% returns or a crash of 35% or more is more likely. But 10-year expected returns on zero percent would undoubtedly decimate managed funds and individual portfolios.

“It’ll Be An Avalanche”

Peters is on record stating that a crashing global “credit impulse” is likely to result in steep market declines. He even predicted an exact date: Valentine’s Day 2018. Talk about forecasting.

While we shy away from giving specific market timelines, his point about declining credit impulses imploding the market is interesting. While Peters was referring to global credit contraction, declining domestic commercial loan growth has proven to be a successful recession predictor.

Case in point: negative Commercial and Industrial (C&I) loan growth has accurately forecast the last eight recessions, dating back to the 1960s. Right now, after years of advances, it’s threatening to go negative. The importance of this metric is simple: without a continuous influx of borrowing (new loan creation), the economy grinds to a halt. Real organic growth stemming from outright purchasing based on savings is dead. Few companies are flush with enough cash to build factories or purchase vehicle fleets without relying almost wholly on debt.

This is problematic for a couple of reasons. First, any semblance of “strong” economic activity is now entirely based on ultra-low interest rates. Should they normalize to historical averages, the economy is cooked. People and corporations have little ability to take on more debt—let alone at higher interest rates. Second, rising debt-to-equity ratios are unsustainable in the long run. When they expand, it leads to even steeper recessionary impulses from the subsequent debt hangover. None of this leads to sustainable economic growth with “normal” breaks in the business cycle.

If Peters is correct, the coming stock market correction could be a doozy. High market valuations and crashing earnings are toxic to rising stock market indices. We’re getting closer to that destructive inflection point.